Reinforcement Learning for Portfolio Optimization

Overview

This project involves optimizing the objectives of portfolio management via a deep reinforcement learning model. The algorithms involves a multi-sequence, attention-based neural-network models tailored to financial data that is based off of the AlphaPortfolio model, which is outlined here.

Problem Statement

Portfolio construction and management is a very important and difficult part of finance. It requires making allocation decisions under uncertainty. Given the high-dimensional, noisy, and nonlinear nature of financial and economic data, traditional methods (in machine learning especially) can have serious drawbacks. The task of this competition is to use an agent/critic reinforcement learning algorithm to optimize portfolio construction given a set of assets. With the complexity of financial data, searching using trial-and-eror through a flexible modeling space to directly maximize a portfolio management objective can be more effective than attempting to estimate prices or returns directly and then prescribing portfolio weight based on that. Attention-based modeling can also improve capturing long-term memory and nonlinearity.

Technical Approach

Model Approach

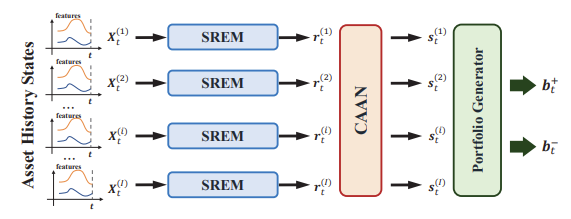

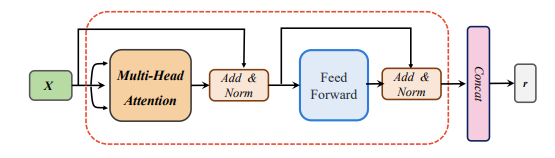

Overall, the model consists of two main architectures: the portfolio generator architecture and the RL architecture. The portfolio generator architecture is taken directly from the AlphaPortfolio model, which includes using sequence representation extraction models (SREMs) to extract a representation for each asset in its state history. In this case, a transformer encoders are used as the SREMs. For more reading on transformers, one can look at my S&P 500 Betting with Transformers project. Then, those representations are sent into a Cross-Asset Attention Network (CAAN) which takes the representations of all assets as inputs to extract relationships among the assets. Lastly, the final portfolio generator takes the scalar winner score for every asset from CAAN and derives the optimal portfolio weights.

Figure 1: The overall architecture of the portfolio generator. Taken from 1.

Figure 2: The architecture of the Transformer Encoder. Taken from 1.

This architecture is embedded into a reinforcement learning framework to train the model parameters to maximize an evaluation criterion. This project uses an actor-critic objective minimizing temporal difference (TD) error while maximizing advantage-weighted actions, regularized by a global Sharpe ratio bonus.

Results & Impact

This project is still ongoing and results will be posted once completed.